Impact on Recipient for non-payment of tax by the Supplier

Rule 37A. Reversal of input tax credit in the case of non-payment of tax by the supplier and re-availment thereof :

Background of Introducing Rule 37A of CGST Rules, 2017:

Prior to the implementation of this Rule, suppliers would report their transactions in Form GSTR-1, allowing buyers to view these details and avail of Input Tax Credit (ITC) in their GSTR-2B. However, suppliers often neglected to file their GSTR-3B returns or failed to remit the actual tax amounts to the government. Consequently, buyers, having already paid the full invoice value to the suppliers, claimed ITC in good faith based on the matching provisions. When discrepancies surfaced, the GST Department required buyers to reverse the ITC, along with additional interest, due to the suppliers’ non-payment of taxes. This led to significant financial setbacks for buyers who had no control over the suppliers’ compliance.

Furthermore, there was no mechanism to reclaim these credits in GST returns even after the suppliers eventually paid the tax. The introduction has ensured that the taxpayer will get the credits once the supplier has paid the tax.

What is Rule 37A of CGST Rules 2017:

- Supplier has issued the invoice/debit note for goods/services and also reported in GSTR-1 but failed to file GSTR-3B and also failed to pay tax.

- Recipient has accounted the invoice/debit note and availed the ITC based on Matching provisions as per GSTR-2B.

- Now since supplier has not filed GSTR-3B, recipient has to reverse the ITC availed earlier through Table 4(B)(2) for form GSTR-3B.

Time limits to reverse the ITC as per Rule 37A:

| Condition | Whether ITC to be reversed | Interest Applicability | ||||

| If Supplier filed GSTR-3B on or before 30th September of the year following the financial year. | Not required to reverse the ITC which has been claimed earlier | Not applicable | ||||

| If Supplier filed GSTR-3B after 30th September of the year following the financial year. | ITC needs to be reversed in GSTR-3B which has been claimed earlier |

|

Re-claim of ITC reversed under Rule 37A:

- Recipient can re-claim or re-avail the ITC in Table 4(D)(1) of Form GSTR-3B of any subsequent period once the supplier files GSTR-3B and pay the taxes thereon. There is no restriction of time limits for re-claim or re-availment of ITC.

How to identify the Suppliers who have defaulted in payment through GSTR-3B:

- GSTR-2A – List is available for those suppliers who have not filed GSTR-3B

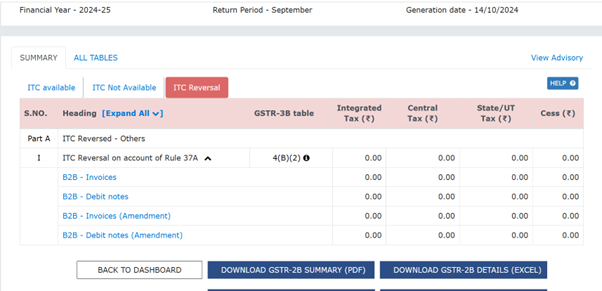

- GSTR-2B – ITC reversal under Rule 37A tab is available

Screenshot where one can find details of ITC reversal on GST Portal

To Navigate – Login to GST Portal -> Services -> Return Dashboard -> Select the month -> View GSTR-2B

Conclusion:

Rule 37A of the CGST Rules has been implemented to ensure compliance and accountability in the Goods and Services Tax (GST) system. Here are the key reasons for its introduction:

- Preventing Revenue Loss: The rule aims to safeguard government revenue by ensuring that Input tax credit (ITC) is only claimed when the corresponding tax has been paid by the supplier. This reduces the risk of fraud and ensures that the system is not exploited.

- Encouraging Timely Compliance: By requiring registered taxpayers to reverse ITC when suppliers fail to file their returns or pay taxes, Rule 37A encourages timely compliance from suppliers. It incentivizes them to adhere to their tax obligations.

- Establishing Clear Mechanisms: The rule provides a clear framework for reversing and re-claiming ITC. This helps taxpayers understand their responsibilities and the procedures they need to follow if suppliers default on their obligations.

- Maintaining Integrity in the Tax System: By linking ITC eligibility to the supplier’s tax payment and compliance status, Rule 37A reinforces the integrity of the GST system. It ensures that only genuine transactions and tax credits are recognized.

- Facilitating Transparency: The requirements under Rule 37A promote transparency in the input tax credit mechanism, making it easier for tax authorities to monitor and audit compliance.

In summary, Rule 37A is designed to enhance accountability within the GST framework, ensuring that tax credits are only available when taxes have been duly paid, thus supporting the overall integrity of the tax system

***