In the world of GST regulations, compounding of offences provides a unique mechanism for defaulters to escape major legal consequences. This article delves into the concept of compounding offences under the GST Act, 2017, elucidating the process, eligibility conditions, compounding charges, and various aspects of classification.

Relevant Legal Provisions under GST:

| Chapter XIX of the CGST Act: Offences and Penalties | |

| Section / Rule | Particulars |

| Section 138 | Compounding of Offences |

| Rule 162 | Procedure for Compounding of Offences |

| FORMS under Chapter XIX of the CGST Act: Offences and Penalties | |

| Form No. | Purpose |

| FORM GST CPD-01 | Application for compounding of Offence |

| FORM GST CPD-02 | Order for rejection / allowance of compounding of offence |

There is no definition of the word “compounding” in the GST Act. As per Black’s Law Dictionary, “Compound” means “to agree for consideration not to prosecute (a crime)”. To put it simple, compounding of an offence is a settlement mechanism, by which, the offender is given an option to pay money in lieu of his prosecution, thereby avoiding a prolonged litigation. Compounding is thus, a legally recognized arrangement, whereby the person charged with an offence is offered the option of avoiding prosecution and imprisonment in lieu of monetary consideration by way of penalty; compounding is essential of a contract between the state and the offender whereby the state secures revenue and the offender secures immunity from prosecution.

Compounding is nothing but sort of a compromise between the defaulter/offender and the department to avoid criminal proceedings and is a punishment outside the Court proceedings.

Section 320 of the Code of Criminal Procedure defines “compounding” as to forbear from prosecution for consideration or any private motive.

Judicial outlook:

- If offence is compounded, it means as if no offence had been committed In Maharashtra Power Development Corpn. Ltd. v. Dabhol Power Company [(2004) 52 SCL 224 BOM HC DB)], Bombay HC held that if offence is compounded, it means as if no offence had been committed in the first place.

- Liberty to approach authority for compounding of offence under sec 138:

Petitioner, a Chartered Accountant, was arraigned as an accused on allegation that he in connivance with other accused persons, had allegedly issued GST invoices without any supply of goods to buyers on commission basis causing loss of more than INR 98 crores. Thus, petitioner was arrested as he has committed an offence under sec 132 of the CGST Act. In such circumstances, petitioner was not entitled to be enlarged on bail, however, he was at liberty to approach authority for compounding of offence under sec 138 of the CGST Act- Calcutta HC in Arvind Kumar Munka v. UOI [CRM No. 10075 of 2019 dated 24.12.2019] – affirmed by Calcutta HC [vide C.R.M. No. 1259 of 2020, dated 28.2.2020]

- No further proceeding shall be initiated in respect of the same offence once the compounding of offences takes place:

Bombay HC in Daulat Samirmal Mehta v. Union of India & Ors. [W.P. No. 471 of 2021 dated 15.02.2021].

- Principle of Disclosure:

Compounding of offence is based on the principle of disclosure as explained by the Hon’ble SC in Union of India v. Anil Chanana [2008 (222) E.L.T. 481 (S.C.)]. To understand this principle, rule 162(8) of the CGST Rules (discussed below), provides that the immunity granted to a person upon compounding of offences can be withdrawn by the Commissioner if he is satisfied that such person had, in the course of compounding proceedings, concealed any material particulars or had given false evidence. Thereupon, such person may be tried for the offence and the provision of the GST Act shall apply as if no such immunity has been granted.

- Application for ‘compounding’ of offences in GST

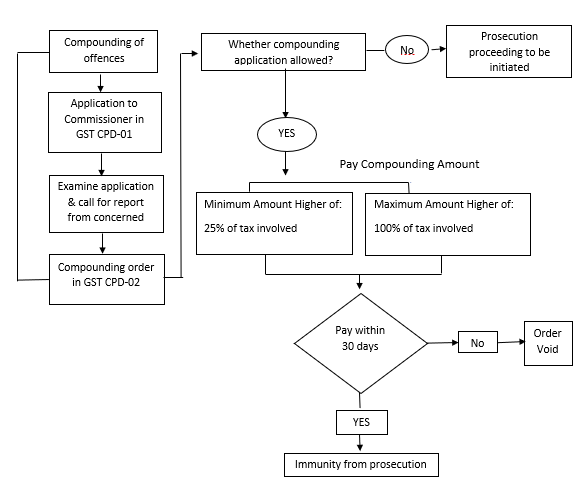

In terms of sec 138(1) of the CGST Act, any offence under GST Act may, either before or after the institution of prosecution, be compounded by the Commissioner on payment, by the person accused of the offence, to the Central Government or the State Government, as the case be, of such compounding amount in the manner prescribed. In this regard, rule 162 of the CGST Rules enumerates below mentioned manner for compounding of an offence:-

- An applicant may, either before or after the institution of prosecution, make an application under sec 138(1) of the CGST Act in Form GST CPD-01 to the Commissioner for compounding of an offence.

- On receipt of the application, the Commissioner shall call for a report from the concerned officer with reference to the particulars furnished in the application, or any other information, which may be considered relevant for the examination of such application.

- After taking into account the contents of the application, the Commissioner may, on being satisfied that the applicant has co-operated in the proceedings before him and has made full and true disclosure of facts relating to the case, by order in Form GST CPD-02, allow the application indicating the compounding amount and grant him immunity from prosecution or reject such application within 90 days of the receipt of the application.

- The application shall not be decided under sub-rule (3), without affording an opportunity of being heard to the applicant and recording the grounds of such rejection.

Amount for compounding of offence

Third proviso to sec 138(1) of the CGST Act read with rule 162(5) of the CGST Rules, provides that compounding shall be allowed only after making payment of tax, interest and penalty involved in such offences.

It is to be noted that the Finance Act, 2023 has reduced the amount for compounding of specified offences except for offence of fake invoicing, by reducing the minimum and maximum amount of compounding.

In this regard, sec 138(2) of the CGST Act provides that the amount for compounding of offences under this section shall be such as may be prescribed, subject to following minimum and maximum amounts:

| Particulars | Amount of penalty |

| Minimum amount for compounding of offences | ►From 01.07.2017 till 30.09.2023:

Higher of – Amount not less than INR 10,000/- (i.e. INR 20,000/- in total for CGST and SGST/UTGST or IGST) or 50% of the tax involved

►W.e.f 01.10.2023:

25% of the tax involved |

| Maximum amount for compounding of offence | ►From 01.07.2017 till 30.09.2023:

Higher of – Amount not less than INR 30,000/- (i.e. INR 60,000/- in total for CGST and SGST/UTGST or IGST) Or 150% of the tax involved

► W.e.f 01.10.2023: 100% of the tax involved |

Further, as per rule 162(6) of the CGST Rules, the applicant shall, within a period of 30 days from the date of the receipt of the order in Form GST CPD-02 by the Commissioner, pay the compounding amount as ordered by the Commissioner and shall furnish the proof of such payment to him

In case, the applicant fails to pay the compounding amount within the time period of 30 days of the order, the order made under rule 162(3) of the CGST Rules, shall be vitiated and be void [rule 162(7) of the CGST Rules].

No further proceedings upon payment of amount:

Sec 138(3) of the CGST Act provides that on payment of such compounding amount as may be determined by the Commissioner, no further proceedings shall be initiated under the GST Act against the accused person, in respect of the same offence and any criminal proceedings, if already initiated in respect of the said offence, shall stand abated.

This principle was upheld in case of PP Varkey v. STO [(1999) 114 STC 251 (Ker HC)] wherein it was observed that once offence is compounded, penalty or prosecution cannot be taken for same offence.

- Cases where compounding of offences is not allowed:

- Specified offences for which compounding is already done once:

Clause (a) to first proviso to sec 138(1) of the CGST Act states that w.e.f 1.10.2023 states that a person who has been allowed to compound once in respect of any of the offences specified in clauses (a) to (f), (h) and (l) of sec 132(1) will not be allowed subsequently for the benefit of compounding of such offences.

The specified offences are as follows:

| Sec | Nature of offence |

| Sec 132(1)(a) | Supply of any goods or services or both without issue of any invoice, in violation of the provisions of the GST Acts and rules made thereunder, with the intention to evade tax. |

| Sec 132(1)(b) | Issue of any invoice or bill without supply of goods or services or both in violation of the provisions of the GST Act, or the rules made thereunder, leading to wrongful availment or utilization of input tax credit or refund of tax |

| Sec 132 (1) (c) | ►For the period 01.07.2017 to 31.12.2020:

Availing input tax credit using such invoice or bill referred to in clause (b) i.e. fake/bogus invoice ►W.e.f. 01.01.2021: Availing input tax credit using such invoice or bill referred to in clause (b) i.e. fake/bogus invoice or bill or fraudulently avails input tax credit without any invoice or bill* |

| Sec 132 (1) (d) | Collecting any amount as tax but failure to pay the same to the Government within a period of 3 months from the date on which such payment becomes due |

| Sec 132 (1) (e) | ► For the period 01.07.2017 to 31.12.2020:

Evading tax, fraudulently availing ITC or fraudulently obtaining refund and where such offence is not covered under clauses (a) to (d) ►W.e.f.01.01.2021 Evading tax, fraudulently obtaining refund and where such offence is not covered under clauses (a) to (d) |

| Sec 132 (1) (f) | Falsifying or substituting financial records or producing fake accounts or documents or furnishing any false information with an intention to evade payments of tax due under the GST Act |

| Sec 132 (1) (h) | Acquires possession of, or in any way concerns himself in transporting, removing, depositing, keeping, concealing, supplying, or purchasing or in any other manner deals with, any goods which he knows or has reasons to believe are liable to confiscation under this Act or the rules made thereunder |

| Sec 132(1) (I) | Attempt to commit or abet the commission of any of the offences mentioned in clauses (a) to (f) above |

- No compounding of offences which are also an offence under any other law:

From 01.07.2017 till the 30.09.2023:

In terms of clause (c) to first proviso to sec 138(1) of the CGST Act, a person who has been accused of committing an offence under GST law which is also an offence under any other law for the time being in force, shall not be allowed the benefit of compounding of such offences.

W.e.f 01.10.2023:

The Finance Act, 2023 has substituted clause(c ) which now read as “ a person who has been accused of committing an offence under clause (b) of sub-section (1) of Section 132”.

By the above amendment, no compounding would be available for the offences under clause (b) section 132(1) i.e. “ issues any invoice or bill without supply of goods or services or both in violation of the provisions of this Act, or the rules made thereunder leading to wrongful availment or utilisation of input tax credit or refund of tax”, would not be eligible for compounding of offence.

- No benefit to a person who has been convicted for an offence under GST Act:

In terms of clause (d) to first proviso to sec 138(1) of the CGST Act, a person who has been convicted for an offence under the GST law by the Court, shall not be allowed the benefit of compounding of such offences.

2. No benefit to a person accused of committing specified offences: From 01.07.2017 till 30.09.2023:

Clause (e) to first proviso to sec 138(1) of the CGST Act states that a person who has been accused of committing an offence specified in clause (g) or clause (j) or clause (k) of sec 132(1) ibid, shall not be allowed the benefit of compounding of such offences.

The above-mentioned offences are as follows:

| Sec | Nature of offence |

| Sec 132(1)(g) | Obstructing or preventing any officer in the discharge of his duties under the GST Act |

| Sec 132 (1) (j) | Tampering with or destroying any material evidence or documents |

| Sec 132 (1) (k) | Failure to supply any information which a person is required to supply under the GST Act or the rules made thereunder or (unless with a reasonable belief, the burden of proving which shall be upon him, that the information supplied by him is true) supplying false information |

W.e.f. 01.10.2023:

It is pertinent to note that sec 132(1) of the CGST Act has been amended vide the Finance Act, 2023 w.e.f. the date yet to be notified, so as to de criminalize the offences specified in clauses (g), (j) and (k) of sec 132(1) of the CGST Act. Accordingly, clauses (g), (j) and (k) of sec 132(1) of the CGST Act has been omitted vide the Finance Act, 2023 w.e.f. from the date to be notified. Meaning there by, any person, who:

- Obstructs or prevents any officer to discharge his duties under the CGST Act;

- Tampers with or destroys any material evidence or documents; fails to supply any information which he is required to supply under the CGST Act or the

- CGST rules or supplies false information

Would not be liable for any prosecution provisions for these specified offences under sec 132(1) of the CGST Act. Hence, no compounding of such specified offences would be required.

However, such person would be liable to penalty of INR 20, 000 (CGST+SGST) or an amount equivalent to the tax evaded or the tax not deducted under sec 51 or short deducted or deducted but not paid to the Government or tax not collected under sec 52 or short collected or collected but not paid to the Government or input tax credit availed of or passed on or distributed irregularly, or the refund claimed fraudulently, whichever is higher, under sec 122 (xiii), (xx) and (xvii) of the CGST Act respectively.

- Any other class of prescribed persons:

In terms of clause (f) to first proviso to sec 138(1) of the CGST Act, apart from above, any other class of persons or offences as may be prescribed, shall also not be allowed the benefit of compounding of such offences.

- Withdrawal of Immunity

Immunity granted to applicant upon compounding of offences, may, at any time, be withdrawn by the Commissioner, if he is satisfied that such person had, in the course of compounding proceedings, concealed any material particulars or had given false evidence. Thereupon, such person may be tried for the offence with respect to which immunity was granted or for any other offence that appears to have been committed by him in connection with the compounding proceedings and the provision of the GST Act shall apply as if no such immunity has been granted [rule 162(8) of the CGST Rules].

In order to make best use of the compounding of offences provisions, it is suggested that at the time of initiating action for launching of prosecution itself, the assessee should be given an offer of compounding. However, the application for compounding will be decided on merits and in exercise of the powers vested with the Commissioner.