The Goods and Services Tax (GST) framework in India increasingly relies on technology to ensure transparency and efficient tax administration. One of the latest technological developments in the GST ecosystem is the Invoice Management System (IMS) introduced by GSTN. The system allows recipients to review invoices uploaded by suppliers and take actions such as acceptance, rejection, or marking invoices as pending before claiming Input Tax Credit (ITC). Recently, GSTN introduced an enhancement in the Outward IMS Dashboard to separately display Rejected Credit Notes, enabling taxpayers to track liability adjustments more efficiently. This article discusses the concept, legal basis, workflow, and technological implications of IMS, along with the role of automation and professional support systems in managing IMS compliance.

- Introduction

GST compliance fundamentally depends on accurate reporting and reconciliation of invoices between suppliers and recipients. Over the years, taxpayers experienced challenges due to mismatches between:

- GSTR-1

- GSTR-2A / GSTR-2B

- GSTR-3B

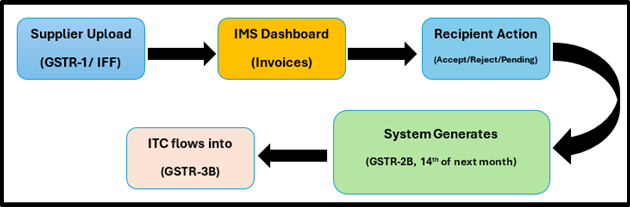

To strengthen the credit verification system, GSTN introduced the Invoice Management System (IMS) effective 1 October 2024. IMS allows recipients to verify supplier-reported invoices before claiming ITC, transforming GST compliance from post-return reconciliation to pre-return validation.

- Legal Framework of IMS

IMS operates within the framework of existing GST provisions.

| Provision | Compliance Impact |

| Section 16(2)(aa) | ITC allowed only when supplier reports invoice |

| Sections 37 & 38 | Provide structure for outward supply reporting and auto-drafted ITC |

| Rule 36(4) | Restricts ITC to system-validated invoices |

| Section 164 | Allows government to prescribe procedural systems |

Thus, IMS does not introduce new legal restrictions but strengthens enforcement through digital verification.

- Concept of Invoice Management System (IMS)

IMS is a technology-enabled verification interface on the GST portal where invoices uploaded by suppliers become visible to recipients for validation.

Recipients can take three actions:

| Action | Meaning | ITC Impact |

| Accept | Invoice verified | ITC available in GSTR-2B |

| Reject | Invoice incorrect | ITC not available |

| Pending | Verification required | ITC deferred |

Invoices with no action automatically become deemed accepted during GSTR-2B generation.

- Documents Not Reflected in IMS

Some transactions bypass IMS and flow directly to GSTR-2B.

| Category | Example |

| Reverse Charge Supplies | RCM invoices |

| ISD distribution | ISD invoices |

| Ineligible ITC | POS restrictions |

| Time-barred invoices | Section 16(4) |

- Recent GSTN Enhancement – Rejected Credit Notes Tab

GSTN recently introduced a dedicated tab in the Outward IMS Dashboard displaying:

Rejected Credit Notes and related records.

Earlier Situation

- Businesses manually tracked rejected credit notes

- Liability adjustments often detected during GSTR-3B filing

New Improvement

Now taxpayers get:

- One-click visibility of rejected credit notes

- Immediate identification of tax liability reversal

Compliance Impact

If a recipient rejects a credit note, the supplier must add back the tax liability in the subsequent GSTR-3B return.

This update significantly reduces manual reconciliation and compliance risk.

- Technology Role in IMS Compliance

IMS creates a technology-first GST environment where companies must adopt automation to manage invoice validation.

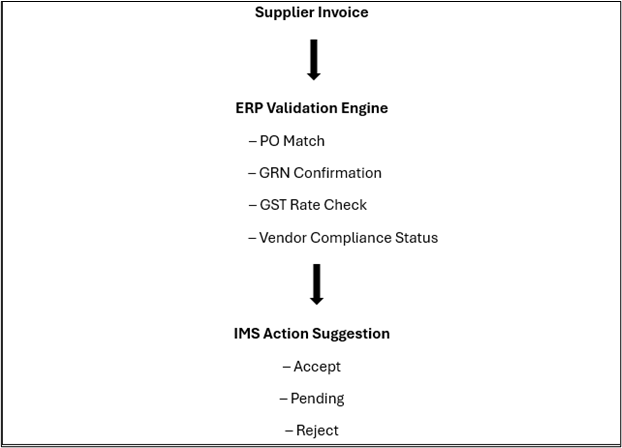

7.1 Automated Invoice Acceptance System

This ensures only legally valid invoices are accepted for ITC.

7.2 Vendor Risk Scoring Model

Automation tools can classify vendors based on compliance behavior.

| Vendor Risk Level | IMS Action | ITC Treatment |

| Low Risk | Auto Accept | ITC allowed |

| Medium Risk | Manual review | Conditional |

| High Risk | Pending / Reject | ITC blocked |

7.3 ITC Reversal and Reclaim Automation

| Event | Automated Action |

| Supplier deletes invoice | ITC auto reversal |

| Supplier re-uploads corrected invoice | ITC reclaim alert |

| Section 16(4) deadline approaching | ITC warning alert |

This protects businesses from ITC loss due to compliance delays.

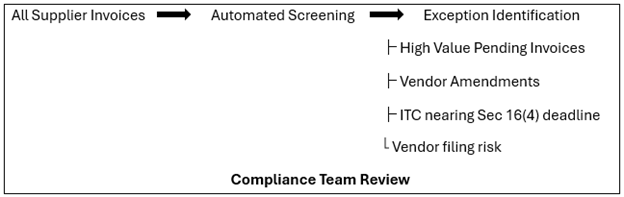

7.4 Exception-Based Compliance Monitoring

Instead of checking every invoice, systems review only exception cases.

This reduces manual workload significantly.

- Bizsolindia Technology Initiative for IMS

As GST compliance evolves toward digital verification, businesses must implement system-driven processes.

To support this transformation, Bizsolindia Services Pvt. Ltd. has collaborated with a technology partner to help organizations implement automation-based IMS compliance systems.

Through this initiative, businesses can access solutions such as:

| Technology Capability | Compliance Benefit |

| IMS dashboard integration | Real-time invoice monitoring |

| Automated validation engine | Prevent incorrect ITC claims |

| Vendor compliance tracking | Identify risky vendors |

| ITC deadline alerts | Avoid credit loss under Section 16(4) |

| Credit note monitoring | Track liability adjustments |

Our team at Bizsolindia can assist organizations in:

- Designing IMS compliance SOPs

- Implementing ERP-integrated validation systems

- Creating vendor communication frameworks

- Establishing audit-ready documentation trails

- Handling of end-to-end IMS compliances

This approach helps companies transition from manual reconciliation to automated GST compliance management. You can drop a requirement mail on corporate@bizsolindia.com for this solution.

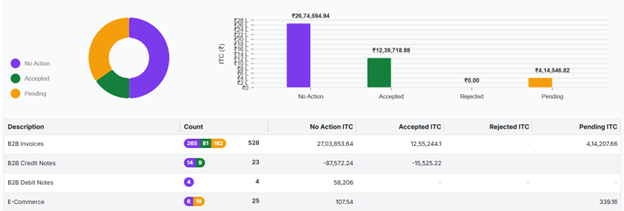

Snapshot of IMS dashboard of “Bizsol IMS Solution”

- Future Compliance Outlook

The GST ecosystem is steadily evolving toward data-driven compliance monitoring.

With continuous enhancements such as:

- IMS

- Real-time invoice validation

- automated ITC statements

- AI-based compliance analytics

Businesses should expect increased system-driven compliance requirements in the coming years.

Organizations that adopt automation and structured IMS monitoring early will be better positioned to manage the future GST environment efficiently.

- Conclusion

The Invoice Management System (IMS) represents a significant milestone in the evolution of GST compliance in India. By enabling recipients to validate supplier invoices before claiming ITC, IMS enhances transparency, reduces mismatches, and strengthens the integrity of the GST credit chain.

The new GSTN enhancement introducing a separate tab for rejected credit notes further simplifies supplier liability monitoring and improves compliance efficiency.

However, the real impact of IMS will be realized when businesses integrate automation tools, vendor risk monitoring systems, and exception-based compliance dashboards into their internal processes.

In the modern GST ecosystem, technology-driven compliance is no longer optional—it is essential.

***