CBIC on recommendation of 53rd GST Council meeting has issued Circular No. 212/6/2024 dated 26th June 2024. The first reaction of Accounts Executive in the Company is “Ohh Teri” “My responsibilities have grown, but my pay hasn’t.” 😊. On the other hand, CA / CMA professionals must be happy for new avenues of business.

Besides lighter part, the question came to my mind why Government issues such incomplete clarifications which creates room for field formation to raise objections.

Legal Framework Governing Reduction of GST Liability for Post Sales Discounts

The issue emerged from the provision of sub-section (3) of section 15 of CGST Act, 2017 wherein is stipulated that, discounts offered by the supplier, through credit notes with GST, will not be formed part the taxable value only if the condition of clause (b)(ii) of sub-section (3) of section 15 is fulfilled. It means for reduction of GST liability against credit notes issued for discounts by the supplier following conditions to be fulfilled:

- Such discount is established in terms of an agreement entered into at or before the time of such supply;

- Such discount must be specifically linked to the relevant invoices

- Input Tax Credit attributable to such discount on the basis of document issued by the supplier has been duly reversed by the recipient.

As there is no functionality/ facility presently available on the common portal to enable the supplier or the tax officer to verify the compliance of the said condition of proportionate reversal of input tax credit by the recipient, burden is shifted on taxpayers to provide CA/CMA certificate or declaration by recipient.

The supplier is required to obtain a certificate from the recipient of supply, issued by the Chartered Accountant (CA) or the Cost Accountant (CMA), certifying that the recipient has made the required proportionate reversal of input tax credit at his end in respect of such credit note issued by the supplier.

In case tax amount in credit note issued for discount in a financial year is less than Rs. 5 lacs, then instead of CA/CMA certificate, the supplier may procure an undertaking/ certificate from the recipient that the said input tax credit attributable to such discount has been reversed by him.

There is no clarity given in the circular, whether such threshold of Rs. 5 lacs will be seen credit note wise or recipient wise or in totality. There is possibility that GST offer may take this threshold in totality basis (all credit notes of all recipients) and deny declaration obtained by the supplier from particular recipients where tax amount of credit notes in financial year for a said recipient is less than five lacs. In my view, this threshold to be seen by recipient wise and declaration of ITC reversal to be obtained from reach recipient where tax amount of credit note is less than rupees five lacs.

Contents of Certificate/Declaration:

The following information must be included in the CA/CMA certification or declaration from recipient:

- the details of the credit notes,

- the details of the relevant invoice number against which the said credit note has been issued,

- the amount of ITC reversal in respect of each of the said credit notes along with the details of the FORM GST DRC-03/ GSTR-3B through which such reversal of ITC has been made by the recipient.

Applicability of circular for CN issued for the reasons other than discounts

It is pertinent to note that this circular is issued only for the credit notes issued for post sales discounts and not for any other reasons. For example, if credit note with GST is issued for sales return or rate difference or short quantity supplied or cancellation of invoice, providing evidence of reversal of ITC by submitting CA/CMA certification or declaration from recipient is not contemplated.

GST officers if demanding CA/CMA certificates / declaration in case of credit notes issued any other reasons than discounts would neither be backed by this Circular nor provisions of GST law.

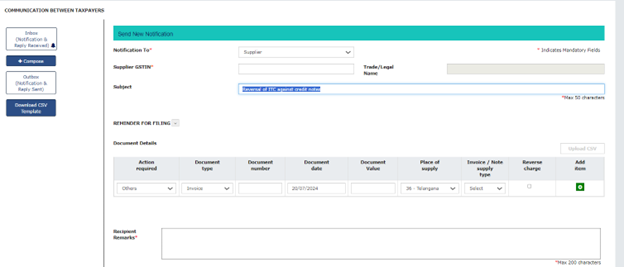

Improving taxpayers communication feature at GST portal:

GST portal has already enabled the feature of communication between taxpayer (refer above screenshot), which can be used for getting confirmation from recipients for reversal of ITC against credit notes issued by the supplier. While composing the communication, GST portal can fetch the credit notes issued by the supplier in the document details and it can be sent to recipients for confirmation. This will be easier than obtaining separate CA/CMA certificates/Declarations from recipients.

It would be an earnest prayer by taxpayers while introducing any additional compliances, good initiatives of Government “ease of doing business’ shall be kept in mind.

Thank you.